If I were to ask you if a sixteen-year-old should open a

Roth IRA, would you agree? As long as that teenager is earning an income and

living with mom and dad, I would highly recommend him or her to open a Roth.

Imagine if that teenager learned the value of compound interest and the power

of time value of money. These two components of financial stewardship are so

important that teaching your son or daughter early that doing so will position

him or her for a comfortable retirement. That is why every time I am asked this

question, I always answer “Now is never too early to start. So, let me give you

the question and follow it with my recommendation.

How early should I begin

planning for my retirement?

The easy answer to this complicated question is that as soon

as you ask the question, you should begin planning. If you are wondering when

you should start, then that is a good indication that you are seriously

thinking about retirement. There are so many demands on a young person’s

financial resources that retirement planning to a young person is “something

that old people do.” However, retirement planning is not something that should

wait. From the day a person enters the workforce, he or she has access to one

of the greatest wealth building resources in the world; an income. The next

best wealth building resource is the company sponsored 401k or 403b plan.

Retirement planning should begin the moment a person has

access to a company sponsored retirement plan. With the death of the

traditional pension, employees are assuming more responsibility for their

retirement and with Social Security on life support, this trend will continue. This

is why more companies are beginning to institute the automatic contribution

program for their employees. According to a report produced by the United

States Department of Labor, approximately 30 percent of eligible workers do not

participate in their employer’s 401(k)-type plan. An automatic enrollment 401k

plan will reduce this number significantly.

Some might ask “What is the benefit of an automatic

enrollment 401k plan?” Well, let’s look at the concept and examine the

benefits. First, an automatic enrollment plan increases plan participation among

both rank-and-file employees and also among managers who might overlook the

benefits of a 401k. Surprisingly, managers who qualify for a 401k don’t take

full advantage of the plan. A company match is a kin to giving yourself a

tax-deferred pay raise. Even contributions made above the company match

simulates a pay raise since ever dollar contributed reduces your taxable

income.

Next, an automatic enrollment plan self-directs

contributions if employees do not select their own investments. Typically,

these self-directed contributions are placed in a targeted date fund, which is

a fancy name for a mutual fund of mutual funds that are weighted based on the

projected retirement date. This feature helps those who are not market savvy have

their money managed for them. As the retirement date approaches, the targeted

date fund adjusts to reduce risk. This feature can also simplify the selection

of investments appropriate for long-term retirement savings for participants.

Finally, these types of programs help employees begin saving

for their future and take advantage of favorable tax treatment. Some companies

are also offering the Roth 401k which takes advantage of tax free growth. The

Roth 401k is a great way for a young person to build significant amounts of

wealth without having the government eventually impact the growth.

Now, to get back to the heart of the question of when should

someone begin to plan for retirement. Honestly, sixteen is not too early to

begin to plan for retirement. Doing this will pay tremendous rewards later on

in life. Some might question the wisdom of planning so early, but keep this in

mind. Life will try, and in many cases succeed, at interrupting your plan.

Therefore, the more time you have built into your plan, the greater number of

interruptions your plan can withstand. When you begin to save for retirement

with ten years to go, a significant financial event will have a greater impact

on your retirement planning.

It is not too early to find an area where you would like to

retire and purchase some land there. If you have the ability to purchase land

(meaning you have the financial resources to pay cash) and you can find the

right location, purchase it now. If you decide later to live somewhere else,

you can always resell the land. Retirement planning isn’t just financial in the

sense that it is all about money. You have to consider where you would like to

live, what activities you want to do, and if there are any special services you

need.

Analytics can be your friend. Knowing what you want out of

your retirement will identify what you need to put into your retirement

planning. One thing I can say with confidence is that I have never met someone

who said “I want to be dependent in my retirement.” We all want a level of

independence and freedom to do the things we never had time to do while we had

to work. Having no plan is having a plan to be dependent. With that said, here

is the time line I suggest for saving for retirement.

When you begin to earn an income in your teens and early

twenties and you don’t have significant expenses, start a Roth IRA. Someone in

his or her teens to early twenties, who can put away $2,000 a year for eight

years has the potential to have $25,736 with a 10.5% return at age 22. If that

person never adds another dollar to the account, he or she could have over $4

million at full retirement age. Therefore, I suggest that anyone in this age

group start the engine of wealth building as soon as he or she can. It only

takes $2,000 a year for eight years.

As you transition from the academic environment to the

working world (between 22 and 30) participate in a company sponsored retirement

plan. Here you can shift from contributing to your Roth IRA to your 401k. If

you have the resources to do both, then by all means, continue to do both, but

the main focus should be on contributing to your 401k up to the company match.

This should always be a part of your wealth building plan so long as you are

gainfully employed.

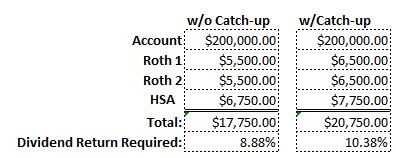

As you enter the child rearing years (30 to 55), continue to

increase your 401k contributions to the maximum IRS limit of $18,000 per year.

In addition to this, max out your Roth each year by contributing the $6,500 IRS

limit. This is the goal. If you cannot reach the limits, contribute as much as

your income and expenses allow. Keeping expenses low means you can keep your

contributions high.

Once your children are grown and raising families of their

own, you can begin to transition to full retirement planning. By this I mean

you can max everything out. Fund 401k contributions and catch-up contributions

to the maximum and do the same for your Roth IRAs. The last 15 employment years

should be the most lucrative contribution years of your life. Granted, these

contributions will see the least amount of growth, but you can benefit from the

tax-treatment in your high earning years.

The process is simple. Start with as much as you can afford

in the early years. Adjust for family needs in the middle years. Close with the

greatest amount of contributions you can in the final years. The truth is that

you should be planning for your retirement from the day you begin to earn

taxable income. By doing this, you will have no need to depend on social

security even though you will still be eligible for it. Be your own security.

Imagine being able to collect social security and donate it to your favorite

non-profit and write it off your taxes when you have to take the MRD from your

IRA.

You can learn more about how to build a powerful retirement strategy by purchasing Simple Wealth Building Strategies or 10 Ways To Improve Your Retirement Planning.