It doesn’t matter if you are 16 or 60, when it comes to

setting financial goals, it is imperative that you position yourself to take

advantage of every opportunity. That means funding every tax favored account

you can to the maximum amount allowed by law. What might surprise you is that

the average income earner can do this with the correct strategy. Most people

lack the ability to lay out a successful strategy when it comes to building

wealth, so I have made it easy for you. If you follow the strategies outlined

in my book, Simple Wealth Building

Strategies, you WILL be able to achieve the following five

financial goals.

The first financial

goal everyone should have is to fully fund his or her employer sponsored

401k account to the maximum allowed by law. For a two income family, that

simply means you will have two solid retirement plans. Current limits are $18K

contribution limit and $6K catch-up contribution for those over age 50. If you

are over age 50, then you need to take advantage of the catch-up contribution. For

most incomes, achieving this goal will require thirty percent or more of your

income. The table below shows two incomes and the required contribution amounts

to successfully save the 401k limit amounts without and with catch up

contributions.

The way to position yourself to accomplish this goal every

year is to stay out of debt. But staying out of debt is not enough. You must also

pay off your mortgage as fast as possible, otherwise you will not have the

flexibility in your income to set aside thirty percent or more. When you are

debt free and you do not have a mortgage, your entire financial world changes. I

don’t want you to think that having this goal is only for rich people. I was

talking to someone the other day who has been working since he was 16 years old

and this year is the first year he will be able to max out his 401k. It has

taken him just over 36 years to reach that point, but he is finally there.

Think about how significant his achievement is. When he began working, 401k’s

didn’t even exist, so he has only been working on this goal since the mid-1980s.

If you want to read an interesting history on the advent of the 401k, click here.

The second financial

goal everyone should have is much like the first. Set a goal to fully fund your

individual Roth IRA accounts. I say accounts for those who are married. Even if

you are a single income family such as mine, you must make it a priority to

first fund the non-working spouses Roth IRA and then your own. Current limits

are $5.5K per individual and $1K catch-up contributions for those over age 50. Once

again, if you are over age 50, then you need to take advantage of the catch-up

contribution. I recommend that the working spouse in a single income family

funds the non-working spouse’s Roth IRA first because the working spouse will

likely have access to an employer sponsored 401k plan that will be fully

funded. The priority is first the 401k, then the non-working spouse’s Roth IRA

and then the working spouse’s Roth IRA. If both people are working, then this

goal is a lot easier, but even for the single or the single income family,

there is a way to build a strategy to do this without impacting the family

budget.

In today’s world of high health care costs and the disaster

known as the “unaffordable care act,” families today need every advantage they

can get. Even individuals need to take advantage of the Health Savings Account

or HSA, as they are commonly called. Therefore,

the third financial goal everyone should have is to fully fund the family’s

HSA. Current limits are $6.75K per

family and $1K catch-up contributions for those over age 55. If you are over

age 55, then you need to take advantage of the catch-up contribution. Don’t

ever leave money on the table when you are in full blown wealth building mode. Some

of you might be asking “How is a family supposed to afford all of this savings

and investments on an average salary?” You have to develop the mentality that

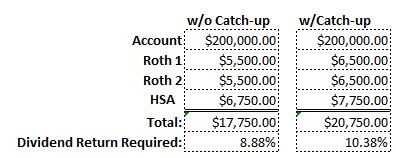

believes “Where salary leaves off, strategy takes over.” The following table

shows that, with a little nest egg, one can use the growth of such to create an

ulterior income that becomes the pump-primer for the well of wealth.

The more you can increase the brokerage account’s value, the

lower the dividend yield you need to accomplish your goal. It is conceivable

that you can get to the point where your money is making more for you than you

make for yourself, but I’ll leave that for another discussion. This goal is a powerful

one, but when you coupe it with the fourth goal, you have a wealth building

engine that will blow you away.

The fourth financial

goal everyone should have is to contribute the same percentage of his or

her income towards the brokerage account that he or she needs to generate in

returns to fund his or her Roth IRA’s and HSA. In the first example, the income

earner must generate an 8.88 percent return to fully fund the Roth IRA’s and

the HSA. Now imagine if the income earner could put an additional 8.88 percent

of his or her income into the brokerage account. Funding the accounts mentioned

would be a lot easier. The key is to use a portion of your current income as

the inorganic seed in concert with your brokerage account to fully fund your

Roth IRA’s and HSA. It is not uncommon to find someone who uses this strategy

contributing 30 percent of his income to his 401k and 11 percent of his income

to his brokerage account. Maxing out your 401k and seeding your brokerage with

inorganic growth can go a long way to achieving these five financial goals.

The fifth financial

goal everyone should have is to increase cash reserves. These cash reserves

are not held in a traditional savings account. This is money you hold in actual

cash. The best way to increase this cash reserve is to identify Passive Revenue

Streams (PRS). Passive Revenue Streams are sources of income that are

non-traditional and income that is generated without requiring a considerable

amount of time or energy. The one rule about passive income that you absolutely

must obey is this. Passive Revenue should never cost you financially. It is passive,

meaning that it should not require a lot of time and energy and it is revenue,

meaning that it is an asset, not a liability.

Passive revenue increases your

wealth, it does not deplete it. You must be creative with this goal.

Turn a hobby into a passive revenue stream. I like to write,

so I write books and self-publish. Since the publishing is on demand, I only

pay a small amount of the royalties towards the costs of publishing, but

nothing out of pocket to make my books available. Once I have written the book

and self-published it, there is no more effort required. Book royalties are

truly a passive revenue stream. The key to this goal is to take the passive

revenue and set it aside in cash. This provides you with a quick source of

funds when you need a small amount of money and cannot get to the bank. Keep

the amount of cash you keep on hand reasonable. You don’t want to have tens of

thousands of dollars on hand unless you are expecting a major emergency.

I titled this message “Five Financial Goals Everyone Should

Have” because I believe that everyone can have these goals. It is just a matter

of will. You should have them, you can have them, but the questions is, do you

WANT to have them? I can tell you that when you do have them and you are

succeeding at achieving them, you will experience life from a different perspective.

While others are panicking about their future, you will be in a totally

different place. A calm place. A place that feels peaceful rather than

stressful.

As a financial stability life coach, I help others develop

strategies that build wealth. Everyone’s situation is different. Therefore, I

do not believe in a cookie-cutter approach to helping others build wealth. You

have to incorporate a fair amount of longitude and latitude in every strategy.

Having margin allows you to capitalize on opportunity that appears when you

have a greater amount of stability. If you are interested in what a financial

stability life coach can do for you, click here.

No comments:

Post a Comment